If you’ve recently been in a car accident, you might hear an insurance adjuster mention “Formula 17c.” This is the standard diminished value 17c calculator they use to quickly estimate how much your car’s resale value has dropped after repairs. But what they often don’t explain is that this formula is designed for their convenience, not to reflect your actual financial loss.

This guide will break down how the 17c formula works, why it often results in a lowball offer, and how you can fight back with the right evidence to get the fair compensation you deserve.

The Insurer’s Starting Point: What is Formula 17c?

When an insurance adjuster uses Formula 17c, they are following a standardized, three-part process. It’s built to ensure speed and consistency for them—not to accurately calculate the drop in your car’s value after an accident.

Think of their calculation not as a final number, but as the insurance company’s opening offer. Understanding how they arrive at that number is the first step in building a much stronger case for the money you’re actually owed.

This formula originated from a 2001 Georgia court case, Mabry v. State Farm, and has been an industry tool ever since. Insurers start with your car’s pre-accident value, apply a 10% cap to establish a “base loss,” and then reduce that amount further with damage and mileage multipliers.

You can learn more about how this fits into the bigger picture by reading our guide on what a diminished value claim is.

How Insurers Break It Down

The calculation might look complicated, but it boils down to three core steps designed to systematically reduce your payout. Here’s a quick overview of how the formula works.

How Formula 17c Works at a Glance

| Step | What It Means | How Insurers Calculate It |

|---|---|---|

| 1. Base Loss of Value | This is the absolute maximum loss they’ll even consider. | Capped at 10% of your car’s pre-accident market value. |

| 2. Damage Multiplier | They apply a penalty based on how bad the damage was. | A rating is assigned for minor, moderate, or severe structural damage, which reduces the base loss. |

| 3. Mileage Multiplier | They apply another penalty based on your car’s mileage. | An adjustment is made for higher mileage, which further decreases the final number. |

As you can see, this rigid, formulaic approach ignores what real-world buyers care about—like the fact that a vehicle now has an accident on its history report. That’s a major factor for a potential buyer, but it’s just a footnote in the insurer’s math. Learn more about diminished value 17c calculator.

Key Takeaway: The 17c formula is a tool for the insurance company, designed to produce a low, consistent number. It’s their opening bid, not the final settlement.

This is exactly why their initial offer is rarely the end of the story.

A Real-World Look at the 17c Calculation

To understand why the diminished value 17c calculator is so problematic, let’s walk through a common scenario. This will show you exactly how an insurance adjuster lands on that first, often disappointing, offer.

Imagine you own a popular SUV with a pre-accident market value of $30,000, based on a trusted source like Kelley Blue Book. The accident caused moderate damage to the frame, requiring significant bodywork.

Starting with the Base Loss Cap

The first thing the adjuster does is apply a 10% cap. This is the absolute maximum loss they will consider from the start.

- $30,000 (Pre-Accident Value) x 0.10 (10% Cap) = $3,000

Instantly, the most you could possibly get under their formula is capped at $3,000. It doesn’t matter if your vehicle is a high-demand model or if the market recoils at its new accident history. This first step immediately puts a low ceiling on your claim.

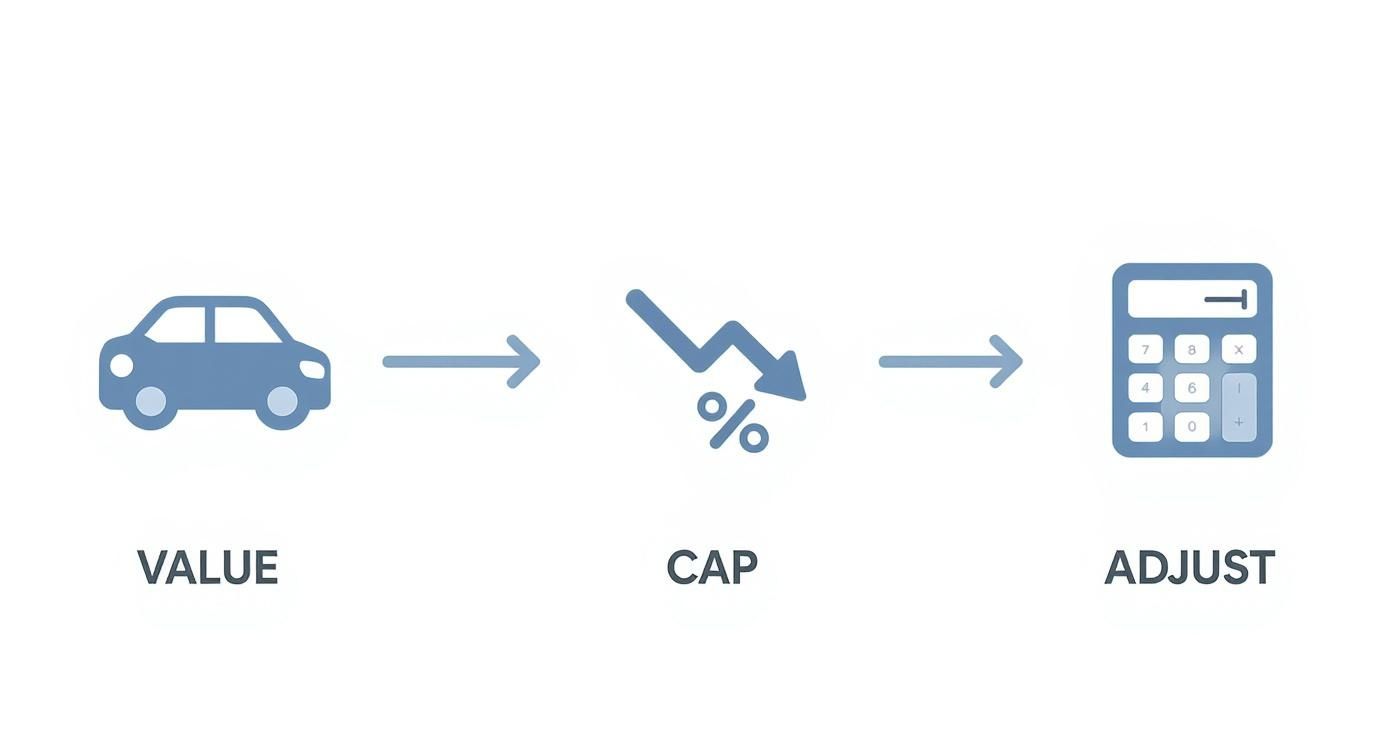

This visual shows the basic flow an insurer follows—starting with your vehicle’s value, applying the cap, and then chipping away at it with more adjustments.

As you can see, the whole process is engineered from the start to systematically shrink the payout.

Applying the Damage and Mileage Multipliers

Next, the adjuster applies two “multipliers” that slash the claim amount even further. These are based on subjective scales that often don’t reflect the true severity of the damage or your car’s actual condition.

1. The Damage Multiplier: Insurers assign a value here based on how bad the repairs were. For our example with moderate structural damage, they’d likely assign a multiplier of 0.50.

- $3,000 (Base Loss) x 0.50 (Damage Multiplier) = $1,500

Suddenly, that $3,000 maximum loss is cut in half. The formula treats complex frame repairs with the same blunt math as a few cosmetic touch-ups—it just uses a different number.

2. The Mileage Multiplier: Finally, they “adjust” for your vehicle’s mileage. Let’s say your SUV has 45,000 miles. On the standard 17c chart, this puts you in a category with a 0.60 multiplier.

- $1,500 x 0.60 (Mileage Multiplier) = $900

After starting with a $30,000 vehicle that took a significant hit, the final offer from the insurer’s diminished value 17c calculator is a mere $900. This amount doesn’t come close to covering the actual loss in value you’d face when trying to sell a car with an accident on its record.

The Bottom Line: The 17c formula isn’t a tool for finding fair market value. It’s an internal insurance process designed to minimize payouts using arbitrary caps and subjective penalties.

This calculation is precisely why you can’t just accept the insurer’s first offer. You need to come back with independent, data-driven proof of your actual loss. A certified appraisal from SnapClaim provides the hard evidence you need to fight for what you’re really owed.

Why the 17c Calculator Often Falls Short

You’ve seen the math behind the diminished value 17c calculator. It feels rigid because it is. This formula wasn’t built for accuracy; it was designed for the insurer’s convenience.

Think of it as a system built to produce a predictable, low number. It’s an opening offer that heavily favors the insurance company, using arbitrary caps and generic multipliers that don’t reflect how real car buyers think. Let’s look at exactly where this formula goes wrong.

The Arbitrary 10% Cap

The biggest issue is the 10% cap. This rule states that no car—no matter how valuable or in-demand—can lose more than 10% of its value from an accident. That’s simply not how the real world works.

Imagine a luxury sedan or a high-demand truck with significant collision damage. A savvy buyer won’t just ask for a 10% discount; they’ll often demand a much steeper reduction, sometimes in the 20-30% range. The 10% ceiling ignores this market reality, unfairly gutting your claim from the very first step.

Key Takeaway: The insurer’s calculation is just an opening offer. It’s an offer you have every right to challenge with real-world evidence of your car’s actual loss in value.

One-Size-Fits-All Adjustments

The problems continue with the damage and mileage multipliers, which are generic and fail to account for your car’s unique details.

Damage Multipliers: The formula treats all “moderate” damage the same. It doesn’t distinguish between damage to a critical frame component versus a replaceable body panel. Real buyers care deeply about the type of damage, not just the repair bill.

Mileage Multipliers: The formula penalizes vehicles for mileage, even though mileage is already factored into the car’s pre-accident value. A car with over 100,000 miles often gets zero for diminished value. An older, well-maintained vehicle absolutely loses value from an accident stigma.

Simply put, the 17c formula is a blunt instrument. It tries to solve a complex problem with a simple, insurer-friendly equation.

Formula 17c vs. Real Market Value

| Factor | Formula 17c Approach | Real Market Approach |

|---|---|---|

| Starting Value | Caps the maximum loss at 10% of NADA value, regardless of the vehicle. | Starts with the vehicle’s actual pre-accident market value, with no artificial caps. |

| Damage Severity | Uses a generic multiplier (e.g., 0.50 for moderate damage) that ignores the type of damage. | Analyzes the specific nature of the damage (structural vs. cosmetic) and its impact on buyer perception. |

| Market Demand | Ignores whether a vehicle is high-demand, rare, or a luxury model. | Considers brand reputation, model desirability, and local market trends. A wrecked Porsche takes a bigger hit than a wrecked sedan. |

| Mileage | Applies a penalty multiplier that can reduce the claim to zero for high-mileage cars. | Views mileage as one of many factors, recognizing that even high-mileage cars suffer from accident stigma. |

| Final Result | A predictable, low-ball number designed to minimize the insurer’s payout. | An evidence-based valuation reflecting what a real buyer would pay for a car with an accident history. |

The takeaway is clear: the diminished value 17c calculator is a biased tool. It overlooks the single most important factor: how real buyers in your local market perceive a car with an accident history. An independent appraisal provides the real-world data you need to counter their flawed formula and strengthen your diminished value claim.

How to Build a Case Against the Insurer’s Offer

Think of the offer from a diminished value 17c calculator as the insurance adjuster’s opening bid, not the final word. If you accept it, you’re almost certainly leaving money on the table. The key to a fair payout is building a strong counter-argument backed by evidence that proves your vehicle’s actual loss in value.

Your goal is to present a clear, logical case with hard facts that the adjuster can’t ignore. The first step is to get your paperwork in order.

Gathering Your Core Evidence

Before you can push back on a low offer, you need a solid foundation. These are the documents that prove the “what, where, and when” of the incident.

Here’s the essential paperwork you’ll need to collect:

- The Official Police Report: This provides an unbiased account of the accident and helps establish who was at fault.

- Itemized Repair Invoice: The final, detailed bill from the body shop lists every part replaced and hour of labor, proving how extensive the repairs were.

- Photos and Videos: Clear images of the damage before any repairs are incredibly powerful visual proof.

These documents are your starting point, but they only prove an accident happened and was fixed. They don’t prove the financial hit you took after those repairs were done. That’s where a professional appraisal comes in.

Your Most Powerful Tool: An Independent Appraisal

The single most effective way to fight a lowball 17c offer is with an independent, certified appraisal. While the insurance company uses a generic formula, a professional appraiser uses real-time, local market data to calculate your car’s true post-accident value.

A certified appraisal shifts the conversation. It moves you away from arguing over the insurer’s flawed formula and forces them to confront what your vehicle is actually worth to real buyers in your area. It replaces their opinion with hard data.

A SnapClaim report delivers this court-accepted proof. It doesn’t just pull a number out of thin air; it analyzes sales of comparable vehicles and pinpoints the specific financial damage caused by the “accident history” stigma. This is the kind of evidence adjusters can’t easily dismiss.

By arming yourself with a data-driven appraisal, you’re no longer just asking for more money—you’re proving you’re owed it. From there, you can confidently learn how to file a diminished value claim built on solid evidence.

Proving Your True Loss with a Certified Appraisal

This is how you level the playing field. When the insurance company returns a low offer from their diminished value 17c calculator, you don’t have to accept it. The real power move is to hand them undeniable proof of what your vehicle is actually worth now.

A certified appraisal report is your single most powerful tool. It systematically dismantles the weaknesses of Formula 17c by replacing made-up multipliers with real-world, market-driven evidence.

Moving Beyond Formulas with Market Data

A professional appraisal isn’t just an opinion—it’s court-accepted, data-driven proof. SnapClaim reports ditch generic formulas and focus on what matters: your local market.

Our certified methodology zeroes in on:

- Comparable Vehicle Sales: We analyze actual sales data for cars just like yours in your area, comparing sales of cars with clean histories to those with accident records.

- Accident History Stigma: The report quantifies the exact “stigma” attached to your car’s VIN now that it has an accident on its record—something Formula 17c ignores.

- Specific Damage Analysis: Instead of a generic multiplier, we analyze the nature and severity of the repairs and how a real buyer would react to that specific damage history.

This level of detail is the leverage you need to negotiate for full compensation. You can see more on how this works in our guide to getting a car appraisal after an accident.

The Real Financial Impact

The hit you take from diminished value is almost always larger than insurers admit. While the used car market changes, the black mark of an accident on a vehicle’s history is permanent.

For a car worth $35,000 before the wreck, the true loss could easily be $3,500 to $7,000. That’s 10% to 20% of its value wiped out—far more than the insurer’s arbitrary 10% cap allows. This is why a custom, accurate appraisal is so critical.

A certified appraisal from SnapClaim gives you the confidence to reject a lowball offer. It arms you with the specific, verifiable data needed to prove your case and hold the insurance company accountable for the full amount.

This professional documentation is designed to be clear and defensible, making it an essential part of your negotiation strategy.

Taking Control of Your Diminished Value Claim

Now you see the problem with the insurer’s diminished value 17c calculator. It’s not a tool designed to make you whole. It’s an internal formula built to minimize what they pay out using arbitrary caps and generic multipliers. If you accept their initial offer, you are almost certainly leaving your own money on the table.

So, what’s next? You need to counter their flawed math with undeniable proof of your actual financial loss. The insurer’s offer is just the starting point for a negotiation. Your most powerful tool is a certified, independent appraisal, which shifts the conversation away from their self-serving formula and focuses it on your vehicle’s true, diminished market value.

Your Next Steps to Fair Compensation

You don’t have to be a master negotiator to get a fair settlement; you just need the right documentation. An independent appraisal provides the data-driven leverage to prove your case and hold the insurer accountable for the real loss.

SnapClaim was created to provide this proof, backed by a risk-free guarantee. Our entire process gives you the confidence you need to fight back.

Our Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

This guarantee means investing in professional proof for your diminished value claim is a decision you can make with complete peace of mind. You have everything to gain by challenging a lowball offer generated by a faulty diminished value 17c calculator.

Don’t let the insurance company tell you what your loss is. Take control of your claim with a certified, data-backed report they can’t ignore.

Frequently Asked Questions (FAQ)

Navigating a diminished value claim can be confusing. Here are answers to some of the most common questions vehicle owners have.

Can I claim diminished value if the accident wasn’t my fault?

Yes. In fact, this is the primary scenario where you can file a diminished value claim. The claim is made against the at-fault driver’s insurance company to compensate you for the loss in your vehicle’s resale value, even after it has been fully repaired.

Can I file a diminished value claim if I was at fault?

Generally, no. Your own collision insurance policy is designed to cover the cost of repairs to your vehicle, not the loss of its market value. The main exception is in the state of Georgia, where drivers may be able to file a first-party diminished value claim with their own insurer.

Is the 17c formula the only way to calculate diminished value?

Absolutely not. While insurers prefer the diminished value 17c calculator because it produces low, predictable payouts, it is not the only or most accurate method. Independent appraisers use market-based evidence, analyzing sales of comparable vehicles with and without accident histories, to determine the true loss in value. This method provides the proof you need to negotiate fairly.

How long do I have to file a diminished value claim?

The deadline, known as the statute of limitations, varies by state but is typically two to three years for property damage claims. However, it’s best to file your claim as soon as the repairs on your vehicle are complete. Acting quickly ensures the evidence is fresh and the market data is current, which helps strengthen your claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.