What is diminished value? It’s the loss in your car’s resale price after an accident—even if it’s repaired perfectly. Insurance companies rarely mention it, but this drop in value can cost you thousands unless you file a proper claim

The Simple Truth About Your Car’s Value After an Accident

Picture two identical cars for sale—same make, model, year, and mileage. One has a clean vehicle history report. The other shows it was in a collision. Even if the repairs on the second car are flawless, which one would a buyer choose? Most people will pick the one with no accident history or demand a big discount on the one that was wrecked.

This simple preference gets to the heart of what diminished value is. It’s not just about the quality of the repairs; it’s about the permanent stigma now attached to your car’s vehicle identification number (VIN).

Why Does an Accident History Matter So Much?

Once an accident is on record, a car’s market value takes an immediate hit. Buyers get nervous for a few good reasons:

- Fear of Hidden Problems: What if there’s underlying frame damage or a mechanical issue that the body shop missed? Future surprise repair bills are a major concern.

- Concerns About Safety: Was the car’s structural integrity fully restored to factory standards? There will always be a nagging doubt in a buyer’s mind.

- Lower Future Resale Value: Buyers know that when it’s their turn to sell the car, they’ll face the same skepticism and have to accept a lower price.

This is the core of what is diminished value. The damage history, now permanently stamped on reports from services like Carfax, directly lowers what a future buyer is willing to pay.

Diminished Value at a Glance

| Concept | What It Means for You |

|---|---|

| Market Stigma | Your car is now less desirable to buyers simply because it has an accident history, regardless of repair quality. |

| Permanent Record | The accident is logged against your VIN on reports like Carfax, creating a permanent red flag for future owners. |

| Financial Loss | You are left with an asset that is worth less money through no fault of your own. |

| Right to Recovery | In most states, you have the legal right to be compensated for this loss by the at-fault party’s insurance. |

This isn’t just a theoretical loss; it’s real money taken out of your pocket by the at-fault driver. Your vehicle is now worth less, and you have every right to be made whole for that loss.

To see how this might apply to your specific car, check out our guide on how much an accident devalues a car.

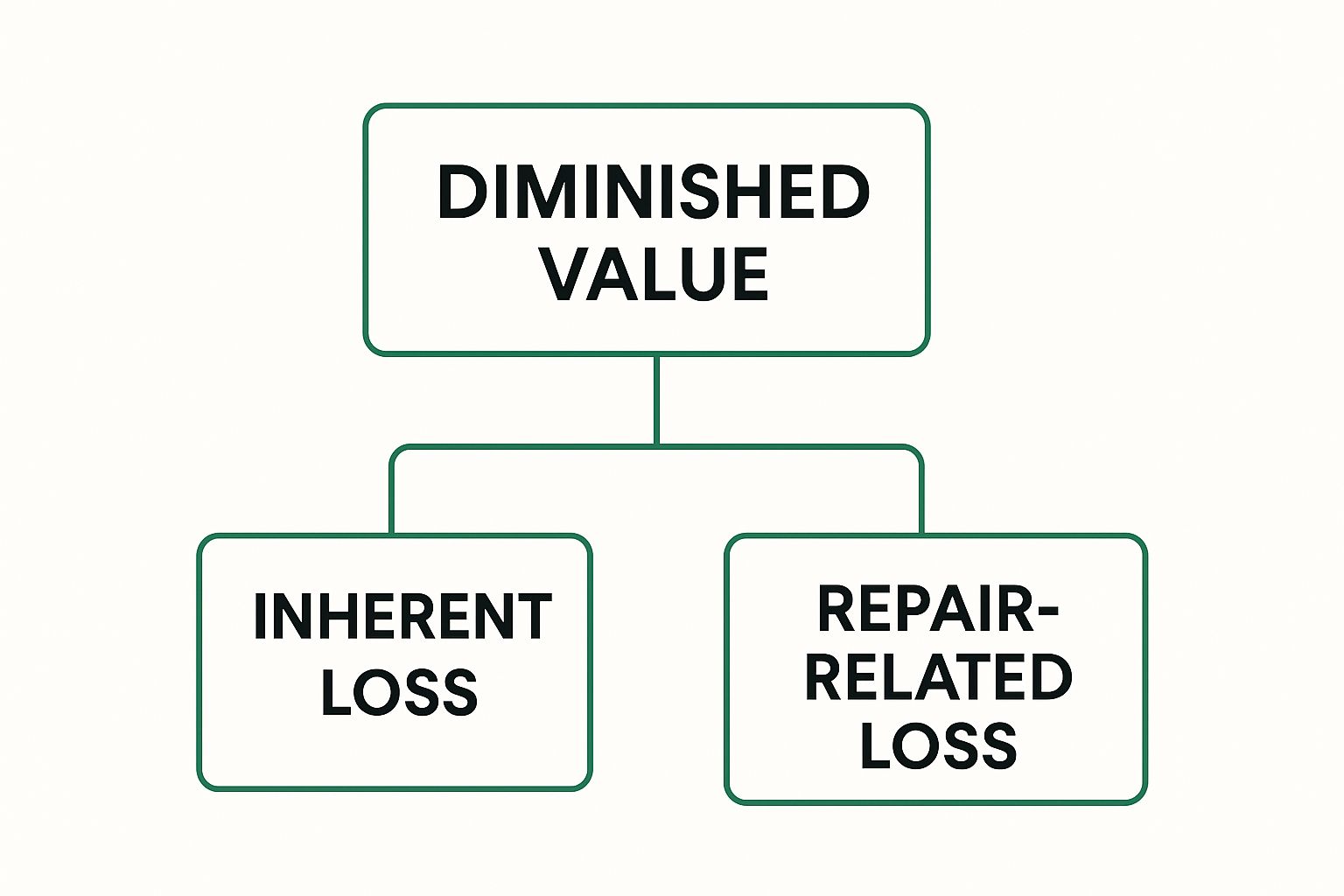

The Three Types of Diminished Value Explained

Not all diminished value is the same. Just as accidents range from minor fender-benders to major collisions, the loss in your car’s value can be broken down into specific types. Understanding these categories helps you pinpoint exactly what kind of financial hit your vehicle has taken and what you’re entitled to claim.

For most drivers, these losses fall into two main buckets: inherent and repair-related.

As you can see, the loss comes from both the permanent black mark of the accident and any shoddy work done during the repairs. Let’s take a closer look at what each of these means for you.

Inherent Diminished Value

Inherent diminished value is the automatic, unavoidable drop in market value that happens simply because your vehicle now has an accident history. This is the most common type of diminished value claim.

It doesn’t matter if the best body shop in the state made your car look brand new. The moment an accident gets logged on a vehicle history report like Carfax, it creates a permanent “stigma.” Any savvy buyer will always pay less for a car with a checkered past compared to an identical one with a clean record.

Key Takeaway: Inherent diminished value isn’t about the quality of the repair. It’s the loss caused by the accident history itself—a blemish you can’t erase. This loss is real, immediate, and can be calculated.

Repair-Related Diminished Value

While inherent diminished value is about the history, repair-related diminished value is about the quality of the repair work. This loss occurs when the repairs are subpar, leaving behind obvious cosmetic flaws or mechanical issues.

Common examples of poor repairs that hurt your car’s value include:

- Mismatched Paint: The new paint job doesn’t quite blend with the original factory finish.

- Aftermarket Parts: Cheaper, non-original (OEM) parts were used, which can compromise the vehicle’s integrity, safety, and value.

- Poorly Aligned Panels: Gaps between the doors, hood, or trunk are uneven and don’t look right.

- Lingering Mechanical Issues: The car no longer drives, handles, or sounds the way it did before the crash.

This type of loss is an additional penalty on top of the inherent diminished value. A professional appraisal is essential to document these specific flaws and give you the proof needed to negotiate with the insurance company.

You might also hear a third term: immediate diminished value. This is the difference in your car’s value right after the accident but before repairs. But since most claims are filed after the car is fixed, inherent and repair-related diminished value are the two types that truly matter. Lean more about what is diminished value claim.

How Insurance Companies Often Undervalue Your Claim

When you file a diminished value claim, you’re asking the at-fault driver’s insurance company to make you financially whole. But their primary goal is to minimize their payout, not to give you a fair settlement.

To do this, many insurers use a flawed, in-house calculation known as the “17c formula.” This formula is designed to produce a low number from the start. It’s their standard playbook, and understanding it is the first step toward challenging their lowball offer.

Unpacking the Problematic 17c Formula

The 17c formula starts by capping your potential loss. It limits the base diminished value at just 10% of the car’s pre-accident NADA retail value. For a $30,000 car, that’s a maximum loss of only $3,000, no matter how severe the damage was.

From there, it applies modifiers that chip away at that value for damage severity and mileage. This rigid, one-size-fits-all approach is a huge red flag, as a newer or luxury vehicle can easily lose far more than 10% of its value after a serious collision.

The Flaw in the Formula: The 17c method applies arbitrary percentage deductions, treating every car the same. It completely fails to consider crucial factors like your vehicle’s make, model, pre-existing condition, or actual demand in your local market.

The formula’s standardized deductions simply don’t capture how real buyers perceive a wrecked-and-repaired vehicle in the marketplace.

Why You Need Independent Proof

Because insurance companies often rely on biased formulas, you can’t expect their first offer to be fair. It’s a number calculated to protect their bottom line, not yours. This is why getting an independent, certified appraisal is so important.

A SnapClaim appraisal provides the unbiased, data-driven evidence needed to push back against a lowball offer. It serves as concrete proof of your car’s actual loss in market value, based on real-world data and expert analysis—not a self-serving formula. This is especially critical when dealing with extensive damage that might lead to conversations about total loss appraisals.

Having a clear handle on the language will only strengthen your position. Ultimately, presenting a professional appraisal report shifts the negotiation in your favor. It replaces the insurer’s opinion with market-based facts, giving you the leverage to demand fair compensation.

What Really Drives Your Car’s Value Down?

Calculating a car’s diminished value isn’t as simple as subtracting the repair bill from its Blue Book price. The real loss is a complex puzzle, with several key factors determining the final amount. Understanding these factors makes it clear why an insurance company’s cookie-cutter formula falls short—and why a professional, data-backed appraisal is your best tool.

A certified appraiser doesn’t guess. They analyze specific criteria to determine the real-world impact an accident has on what a buyer is willing to pay for your car.

The Starting Point: Your Vehicle’s Pre-Accident Value

Before you can measure a loss, you have to establish what your car was worth right before the crash. This baseline comes down to a few core things:

- Make and Model: Luxury brands like Mercedes-Benz, sports cars like a Ford Mustang, or popular SUVs like a Toyota 4Runner often see a much steeper percentage drop in value compared to a standard sedan.

- Age and Mileage: Newer, low-mileage vehicles suffer the most. A two-year-old car with 20,000 miles has far more value to lose than a ten-year-old vehicle with 150,000 miles.

- Pre-Accident Condition: An accurate valuation requires an honest look at your car’s prior condition, from dings and scratches to interior wear and tear.

The Big One: How Bad Was the Damage?

This is perhaps the single most important factor. A minor fender bender is a world away from a collision that deployed airbags or caused structural damage.

If an accident was bad enough to deploy airbags or damage the frame, the diminished value will be significantly higher. Buyers are extremely wary of vehicles with a history of major repairs because it raises long-term questions about safety and reliability.

That damage history becomes a permanent part of your car’s record, flagged on vehicle history reports for any potential buyer to see. This red flag instantly separates your car from identical ones with a clean history, directly impacting its price.

The Wild Card: Market Trends and Demand

Finally, the market itself plays a huge role. The laws of supply and demand for your specific vehicle can either soften the blow or make it worse. For instance, if used car inventory is low and demand is high, buyers might be more forgiving, which can slightly reduce your loss.

All these factors are why a generic online calculator or an insurer’s formula won’t cut it. To get a realistic estimate of your loss, use SnapClaim’s professional diminished value claim calculator for a figure tied to real market data.

Your Step-by-Step Guide to Filing a Claim

Ready to get the money you’re owed? Filing a diminished value claim might seem intimidating, but it’s a straightforward process when you break it down. The key is to build a strong case with undeniable evidence.

Step 1: Confirm You’re Eligible and Gather Your Paperwork

First, make sure you can file a claim. In most states, the rule is simple: you cannot be the at-fault driver. The claim is filed against the other driver’s property damage liability insurance, not your own policy.

Once confirmed, gather these essential documents:

- The Police Report: This officially establishes who was at fault.

- Repair Invoices: The detailed, itemized receipts from the body shop show exactly what was fixed.

- Vehicle History Report: A report from a service like Carfax proves the accident is now on your car’s permanent record.

Step 2: Get a Certified Appraisal Report

This is the most critical step. The insurance company’s initial offer is just their opinion, and it’s almost always low. To negotiate effectively, you need an independent, data-driven report from a certified expert.

A professional SnapClaim appraisal isn’t just a random number; it’s objective, market-based proof of your car’s lost value. Our report analyzes real-time market data, sales trends for your specific vehicle, and the severity of the damage. This report gives you the leverage you need to turn the tables.

Our Money-Back Guarantee Removes the Risk: We are so confident our reports provide the proof needed to strengthen your claim that we back them with a full money-back guarantee. If your insurance recovery is less than $1,000, we’ll refund your appraisal fee. You have nothing to lose by getting the expert evidence you need.

Step 3: Submit Your Claim and Start Negotiating

With your certified SnapClaim report in hand, you’re ready to act. Formally submit your claim to the at-fault driver’s insurance adjuster with a clear demand letter. State that you’re seeking compensation for your vehicle’s inherent diminished value and attach a copy of your appraisal report and all other documents.

Don’t be surprised when the adjuster comes back with a lower offer—they almost always do. This is where your appraisal becomes your best tool. Stand your ground politely but firmly, and refer back to the hard data in your report. The goal is to shift the conversation from their opinion to the facts you’ve presented.

For a more detailed walkthrough, check out our complete guide on how to file a diminished value claim.

Frequently Asked Questions (FAQ)

Stepping into a diminished value claim for the first time can be confusing. Here are straightforward answers to the questions we hear most often.

Can I claim diminished value if I was at fault for the accident?

Generally, no. Diminished value claims are filed against the at-fault driver’s insurance policy as a “third-party claim.” Your own collision coverage is designed to pay for your vehicle’s repairs, not to compensate you for its loss in resale value. The other driver’s insurance is responsible for making you whole for all losses, including diminished value.

How long do I have to file a diminished value claim?

Every state has a legal deadline called the statute of limitations for filing property damage claims. This time limit varies by state but is typically two to three years from the date of the accident. If you miss this window, you lose your right to file a claim, so it’s always best to act quickly.

What if the insurance company uses the 17c formula?

The 17c formula is a flawed, internal calculation some insurers use to produce low settlement offers. It applies arbitrary caps and deductions that don’t reflect real-world market conditions. A certified appraisal report from SnapClaim is your best defense, as it provides market-based evidence that refutes the 17c formula and supports your claim for fair compensation.

Do I need to sell my car to prove I lost money?

Absolutely not. This is a common myth. The financial damage—the diminished value—occurs the moment the accident is recorded on your vehicle’s history. This permanent stigma immediately lowers what any buyer would be willing to pay. You have the right to be compensated for this immediate loss, whether you plan to sell the car tomorrow or drive it for another ten years.

Don’t let an insurance company’s formula dictate what you’re owed. SnapClaim provides the certified, data-driven appraisal reports you need to prove your vehicle’s true loss in value and strengthen your claim. Get a free estimate today or order your certified report to get the fair compensation you deserve.