Has your insurance company declared your car a total loss and made you a settlement offer that seems way too low? You’re not alone, and it’s essential to understand the term they’re using: actual cash value (ACV). Simply put, ACV is what your vehicle was worth on the open market right before the accident, factoring in depreciation from age, mileage, and wear.

Understanding this one concept is the key to getting a fair payout. Let’s break down what ACV means for your claim and how you can ensure you get the compensation you deserve.

What Actual Cash Value Means for Your Claim

Getting a grip on actual cash value is the single most important step toward a fair settlement for your totaled car. Think of it like a five-year-old smartphone—even in perfect condition, it doesn’t have the same value as a new one. ACV applies that same real-world logic to your car, accounting for all its depreciation.

This number is where most of the friction happens between you and your insurer. Their goal is to close your claim for the lowest amount possible, which often leads to an ACV offer that feels shockingly low. Your goal is to get a settlement that truly reflects what your vehicle was worth before the crash.

The Core Components of ACV

The basic formula for actual cash value seems simple, but the details are where insurance companies often undervalue claims. At its heart, the calculation looks like this:

Replacement Cost – Depreciation = Actual Cash Value

Let’s break down what those terms mean in plain English:

- Replacement Cost: This isn’t the sticker price of a new car. It’s the cost to buy a similar used vehicle—same make, model, year, and condition—in your local area.

- Depreciation: This is how much value your vehicle has lost over time due to factors like age, mileage, any prior damage, and its overall condition.

This concept isn’t unique to auto insurance. The gap between an item’s current worth and its replacement cost is a major issue across the industry. For example, between 2014 and 2023, natural disasters caused $2.3 trillion in economic losses, but insurance only covered $944 billion. This left a 60% protection gap, partly because ACV payouts don’t cover the full cost to rebuild. You can read more about these challenges in the 2025 EY Global Insurance Outlook.

Why This Number Is So Important

The ACV directly determines the size of the check you’ll get for your totaled car. If the insurance company’s valuation is too low, you won’t have enough money to buy a comparable replacement vehicle, forcing you to pay the difference out of your own pocket.

That’s exactly why you should never accept the first offer without doing your homework. You have the right to question the insurer’s math and provide your own evidence to support a higher, more accurate actual cash value.

How Insurers Calculate Your Vehicle’s Actual Cash Value

Insurance companies don’t just pull a number out of thin air. They use software and third-party valuation reports to determine your vehicle’s actual cash value, but this process is often flawed and works in their favor.

Understanding how they arrive at their number is the first step toward spotting errors and fighting for a fair payout. These reports are supposed to find your car’s fair market value by comparing it against similar cars sold recently in your area, but they often miss the mark.

The Key Ingredients in Their Formula

An adjuster plugs several key details about your car into their valuation system. Each piece of information nudges the final ACV number up or down.

Take a look at the primary factors that insurers use to calculate your vehicle’s ACV. These are the building blocks of their settlement offer.

Key Factors Influencing Your Vehicle’s ACV

| Factor | Description | Impact on ACV |

|---|---|---|

| Core Vehicle Details | The basics: year, make, model, and trim level. | Sets the baseline value. |

| Mileage | The number of miles on the odometer before the crash. | Lower mileage almost always means a higher value. |

| Overall Condition | The adjuster’s grade of your car’s pre-accident condition (e.g., excellent, good, fair, poor). | Highly subjective and a frequent source of disputes. |

| Options & Upgrades | Features like a sunroof, premium audio, or advanced safety packages. | Should increase value but are often missed or undervalued. |

| Recent Maintenance | Significant work like new tires or a recent major service. | Can add value but is rarely included unless you point it out. |

Once these details are in, the system generates a starting value. But that’s just the beginning—the next step is where things often go wrong for car owners.

The Problem with “Comparables”

The most critical part of an insurer’s valuation is the use of comparables, or “comps.” These are listings of similar vehicles that have recently sold in your local market. The system uses these sales to justify the ACV it calculates for your car.

An adjuster’s report will typically list three to five comparable vehicles. The average selling price of these “comps” is what really drives your final settlement offer.

Here’s the catch: the comps chosen by the insurer’s software are often not truly comparable to your car. This is where many valuations go completely off the rails.

For instance, the report might:

- Use comps with much higher mileage than your vehicle.

- Include cars that were in worse pre-accident condition.

- Pull listings from distant towns where car values are lower.

- Compare your fully-loaded model to a bare-bones base model.

Every one of these flaws will drag down your insurance total loss payout. Learning to spot bad comps is one of the most powerful ways to challenge a lowball offer. You can start by searching sites like Kelley Blue Book or local dealer websites to see what cars like yours are actually selling for.

Why Their Reports Are Often Flawed

At the end of the day, the valuation tools used by insurers are built to standardize the claims process and control costs. They often miss the little details that made your specific car valuable, like its immaculate service history or the brand-new tires you just bought.

Worse yet, these systems often lean on dealer wholesale prices—not the retail price you would have to pay to buy a replacement. This gap is a major reason why an insurer’s first offer often feels insultingly low. By understanding how they build their valuation, you gain the power to take it apart. A good first step is to get a baseline with a trustworthy auto actual cash value calculator.

ACV vs. Replacement Cost vs. Diminished Value

When you’re dealing with an insurance claim, the jargon can get confusing. Three terms often get thrown around—actual cash value, replacement cost, and diminished value—but they mean very different things for your wallet.

Understanding the role each one plays is crucial. One applies when your car is a total loss, another is a rare policy add-on, and the third is for when your car gets repaired but loses resale value. Let’s get them straight so you know what you’re entitled to.

Actual Cash Value: The Standard Payout

As we’ve covered, actual cash value (ACV) is the most common way insurance companies value your vehicle after a total loss. It represents your car’s fair market value the moment before it was damaged, which is the price a real person would have paid for your car in its pre-accident condition.

This calculation is the bedrock of the insurance industry’s financial model. The practice of paying out a vehicle’s depreciated worth—instead of its brand-new sticker price—underpins the $9.7 trillion in assets held by insurers. This approach helps them manage risk and stay solvent. For a look at the industry’s scale, check out stats from the Insurance Information Institute.

Bottom line: if your car is declared a total loss, the ACV is the amount your insurer will offer you, minus your deductible. This is the standard for almost every auto policy.

Replacement Cost: The Uncommon Upgrade

Replacement Cost Value (RCV) is exactly what it sounds like: the amount of money needed to replace your totaled vehicle with a brand-new one of the same make and model. This is a world away from ACV, which only pays you for the used value of your car.

However, RCV coverage is not standard. It’s typically sold as an expensive add-on, or “rider,” to an auto policy and is often only available for new cars. While it provides a much bigger payout, the higher premiums mean most drivers stick with standard ACV coverage.

Diminished Value: The Post-Repair Loss

This is where many vehicle owners miss out on money they are owed. A diminished value claim addresses the loss in your car’s resale value after it has been in an accident and repaired. Even with perfect repairs, a car with an accident history is worth less than an identical one with a clean record.

A diminished value claim is completely separate from a total loss settlement. It only applies when your car is repaired, not totaled. You can’t claim both ACV (for a total loss) and diminished value on the same vehicle.

Imagine your one-year-old SUV gets into a fender-bender. The insurance company pays for repairs, but now its vehicle history report has a permanent black mark. Potential buyers will offer you thousands less than they would have before the crash. That loss in market value is its diminished value, and in most states, you can file a claim to recover that money.

| Concept | When It Applies | What It Covers |

|---|---|---|

| Actual Cash Value (ACV) | Your car is declared a total loss. | The market value of your vehicle before the accident, minus depreciation. |

| Replacement Cost | Your car is a total loss, and you have this special coverage. | The cost to buy a brand-new replacement vehicle. |

| Diminished Value | Your car is repaired, not totaled. | The loss in resale value your car suffers after repairs are completed. |

Knowing which situation applies to you is the first step. If you’re dealing with a total loss, your focus should be on challenging the insurer’s lowball ACV calculation, a process we break down in our guide to total loss vehicle calculations.

Why Your Insurer’s First Offer Is Just a Starting Point

Getting that first settlement offer from the insurance company can be a gut punch. You know what your car was worth, and the number they’ve come back with feels like it’s from another planet.

There’s a simple reason for this: insurers are businesses, and their goal is to minimize what they pay out on claims. Their initial actual cash value offer isn’t a personal attack—it’s just business.

This first number is produced by systems and data that are often skewed in the insurer’s favor. They count on you to be tired, frustrated, and willing to accept it without a fight. You shouldn’t. Think of their offer as the opening bid in a negotiation, not the final decision.

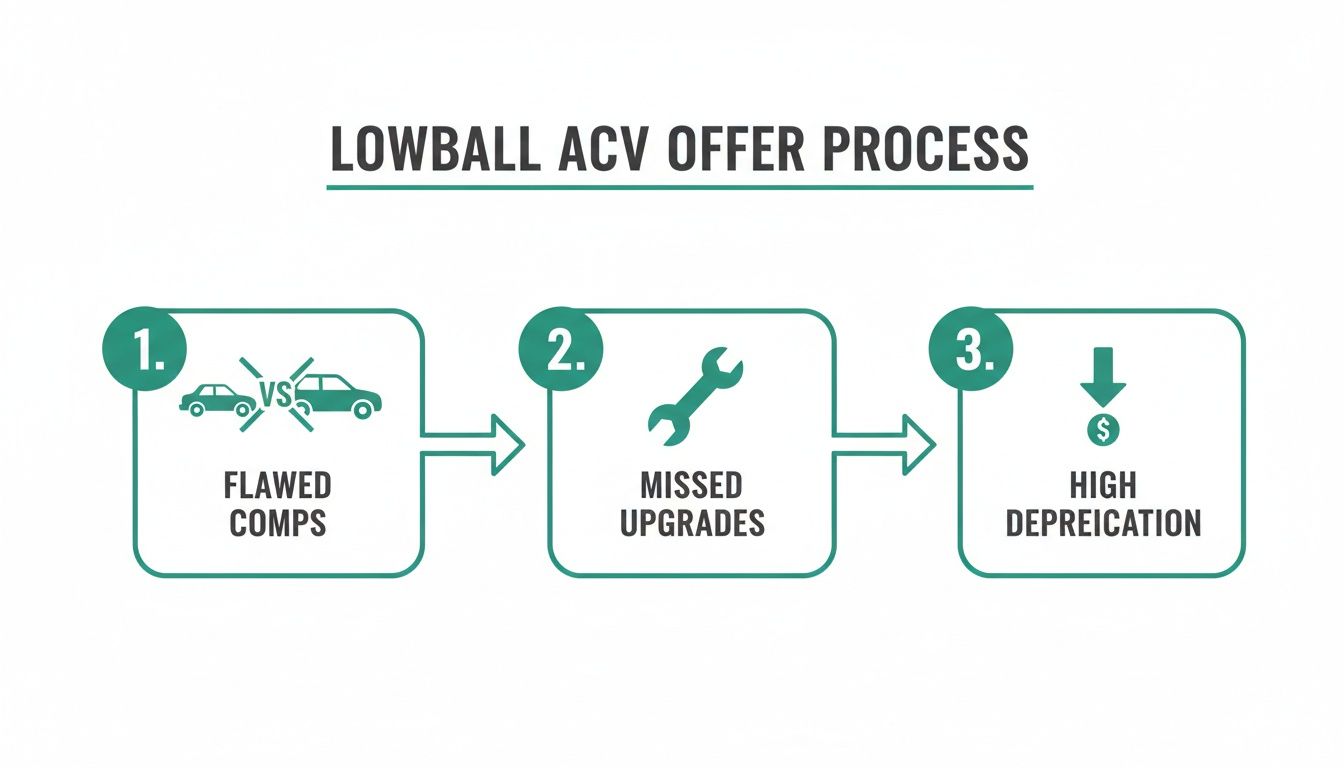

Common Tactics That Lead to Lowball Offers

Insurance adjusters work from valuation reports that can be full of holes. These reports are often auto-generated and easily miss the unique details that made your vehicle more valuable. Knowing their common shortcuts is your first line of defense.

The process often boils down to using bad comparable vehicles, ignoring recent upgrades, and applying excessive depreciation—all of which systematically drive down your payout.

This flowchart shows exactly where an insurer’s valuation can fall short. Here are the three most common tactics to watch out for:

Using Flawed “Comparables”

The adjuster’s report will list several “comps” to justify their number. But look closer. They might use vehicles with far more miles, base models instead of your fully-loaded trim, or even cars from another state where they sell for less.Overlooking Recent Upgrades

Did you just drop $1,000 on new tires? Install a premium sound system? Those things add real value, but they’re almost never in the initial report. Unless you bring receipts and demand they be included, the insurer will conveniently ignore them.Applying Excessive Depreciation

Condition is subjective, and adjusters use that to their advantage. They might label your car’s pre-accident condition as “average” without a real inspection, instantly shaving hundreds or thousands off its value. They also apply generic depreciation that doesn’t account for your vehicle’s excellent maintenance history.

You Have the Right to Disagree

It’s important to remember this: you are not obligated to accept their first offer. Your insurance policy is a contract, and you have every right to dispute their valuation if you have evidence that it’s wrong.

Buried in most auto policies is an “Appraisal Clause.” This clause gives you a formal process to challenge the insurer’s number by hiring your own independent appraiser.

This clause is a powerful tool most people don’t know exists. It levels the playing field by forcing the insurer to consider evidence beyond their own biased reports and is your ticket to negotiating the insurance total loss payout you’re truly owed.

Your Step-by-Step Plan to Dispute a Low Settlement

That sinking feeling when you see the insurance company’s settlement offer is all too common. But you don’t have to just accept a lowball number. The key is knowing how to fight back with a clear, evidence-based strategy.

This roadmap will walk you through the exact steps to challenge the insurer’s math and negotiate for the compensation you’re actually owed. Let’s get started.

Step 1: Request the Official Valuation Report

Your first move is simple: formally ask for a complete copy of the insurer’s valuation report. This isn’t a verbal summary from the adjuster—it’s the official document that breaks down exactly how they calculated your vehicle’s actual cash value.

Getting this report is non-negotiable. It contains the specific “comparable” vehicles and condition adjustments they used, and it’s where you’ll find the errors needed to build your case.

Step 2: Scrutinize the Report for Common Errors

Once you have the report, it’s time to put on your detective hat. You’re looking for mistakes and unfair assumptions that dragged down your insurance total loss payout.

Zero in on these key areas:

- Incorrect Vehicle Options: Did they list your car as a base model when you had the premium trim? Look for missing features like a sunroof, leather seats, or an upgraded engine.

- Unfair Condition Rating: Adjusters love to slap an “average” rating on a car’s pre-accident condition. If your vehicle was in excellent shape, this subjective rating is a huge point of contention.

- Flawed Comparable Vehicles: This is the most common error. Take a hard look at the “comps” they used. Do they have more miles? Are they from a different state where cars are cheaper? Are they missing options that your vehicle had?

A single bad “comparable” can poison the whole valuation. If their comps don’t truly match your vehicle’s specs and condition, their ACV calculation is built on a house of cards.

This isn’t just a car insurance problem. The concept of actual cash value creates huge gaps in property insurance, too. In states like Florida and California, home repair costs have shot up 35% since 2019, while insurance premiums have soared over 31%. For homeowners, an ACV policy on an older roof might only pay a tiny fraction of what a new one costs.

Step 3: Gather Your Own Compelling Evidence

Now it’s your turn. The goal here is to collect concrete proof that refutes the flaws in their report and establishes a higher, more accurate value for your car.

Start gathering these documents:

- Proof of Condition: Pull together recent photos of your car (from before the accident), detailed maintenance records, and any service history reports.

- Receipts for Upgrades: Did you just buy new tires, brakes, or a battery? Find the receipts for any significant purchases or upgrades.

- Your Own Comparables: Head to online auto marketplaces like Kelley Blue Book, Autotrader, and local dealer websites. Find vehicles that are a true match for yours and screenshot those listings as proof.

Step 4: Submit a Counteroffer and Invoke the Appraisal Clause

With your evidence in hand, draft a professional letter or email. Clearly state that you are rejecting their initial offer and present your counteroffer, backed by the proof you’ve collected.

If the insurance company refuses to negotiate, you have a powerful tool in your policy: the Appraisal Clause. This provision gives you the right to hire your own independent, certified appraiser. The insurer then hires their own, and the two experts negotiate a binding settlement. If things get complicated, you might also consider consulting a car accident law firm to advocate on your behalf.

How a Certified Appraisal Strengthens Your Claim

Bringing your own research to the table is a great start, but an independent appraisal from a certified expert completely changes the conversation. It shifts the dynamic from a simple disagreement to a negotiation grounded in hard facts. That’s how you gain the leverage you need to get a fair settlement for your vehicle’s actual cash value.

An independent appraisal is an unbiased, evidence-based analysis from an expert whose only job is to determine what your specific vehicle was actually worth right before the accident.

The Power of an Expert Report

Think of a professional appraisal as the ultimate trump card in your negotiation. It’s a formal, documented assessment that insurance companies are forced to take seriously.

A SnapClaim report systematically takes apart the insurer’s weak valuation by:

- Providing an Unbiased Valuation: A certified appraiser works for you, not the insurance company. Our analysis is based on industry standards and real-world market data, not a cost-cutting algorithm.

- Documenting True Condition: The report will officially document your vehicle’s pre-accident condition, recent upgrades, and meticulous maintenance history—details adjusters often overlook.

- Using Accurate Comparables: Unlike the insurer’s report, which might pull flawed comps, an independent appraisal uses genuinely comparable vehicles to establish a fair market value, which almost always leads to a higher valuation.

A certified appraisal isn’t just another opinion. It’s a professional, data-backed document that provides the proof you need to negotiate on equal footing. It supports your case with the kind of authoritative evidence that is very difficult for an insurance company to dismiss.

Peace of Mind with a Guarantee

We understand that paying for an appraisal can feel like a gamble, especially when you’re already dealing with the financial stress of an accident. That’s why SnapClaim offers total peace of mind with our Money-Back Guarantee.

If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed. We’re confident that our detailed auto insurance appraisals provide the solid evidence needed to strengthen your claim and help you recover the compensation you rightfully deserve.

Frequently Asked Questions About Actual Cash Value

Here are clear, straightforward answers to the questions we hear most often from vehicle owners wrestling with the total loss process.

Can I negotiate the actual cash value with my insurer?

Yes, absolutely. The insurer’s first ACV offer is just their opening bid, not the final word. You have the right to negotiate, but you need to come prepared with credible evidence that your vehicle is worth more. While you can gather your own research, the single most effective tool is a certified, third-party appraisal report that replaces their opinion with documented facts.

What happens if I owe more on my loan than the ACV payout?

This is a tough situation often called being “upside down” on your car loan. When this happens, the insurer’s actual cash value payout goes directly to your lender. You are then responsible for paying off the remaining loan balance out of your own pocket. This is precisely why GAP (Guaranteed Asset Protection) insurance exists—it’s a separate policy designed to cover that exact “gap.”

Can I claim diminished value if the accident wasn’t my fault?

Yes, in most states, you can file a diminished value claim against the at-fault driver’s insurance company. This claim is separate from your own policy and compensates you for the loss in your vehicle’s resale value after repairs. It applies only when your car is repaired, not when it’s a total loss.

Will recent upgrades or excellent condition increase my ACV?

They certainly should, but only if you can prove it. The adjuster’s initial report has no idea you just bought new tires or kept meticulous service records. It is up to you to provide that documentation. A certified appraisal is the best way to formally document your vehicle’s superior condition and upgrades, ensuring those value-adding factors are properly accounted for to get a higher car value after accident payout.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your free total loss value estimate today or order a certified appraisal report to strengthen your insurance claim.