Has your insurance company told you your car is a total loss? Understanding how they calculate its value is the key to getting a fair payout. This process, called a total loss car valuation, determines the exact amount of money you’ll receive to replace your vehicle.

If the cost to fix your car exceeds its pre-accident worth, the insurer will “total it.” This means instead of paying for repairs, they will cut you a check for its Actual Cash Value (ACV)—the price your car could have sold for the moment before the crash.

What is a Total Loss Threshold?

After an accident, the insurance adjuster has one primary question: is it cheaper to repair your car or pay you its value? To decide, they use a specific formula known as the Total Loss Threshold (TLT).

Think of it like deciding whether to fix an old appliance. If a new washing machine costs $500 but repairing your old one is $600, the repair simply doesn’t make financial sense. Insurers apply this same logic to vehicles. Learn more about total loss settlement process and how long does it take.

How the Threshold Formula Works

The TLT is a percentage, usually determined by state law or the insurance company’s internal policies. A vehicle is declared a total loss if the estimated repair cost plus the car’s salvage value (what it’s worth for parts) exceeds this percentage of its ACV.

For example, let’s say your car’s ACV was $15,000 and your state has a 75% TLT. Your vehicle would be totaled if the repair costs reach $11,250 or more.

Key Takeaway: A “total loss” isn’t based on how damaged a car looks. It’s a purely financial calculation that compares repair costs to the car’s pre-accident market value.

This is becoming more common. In 2023, the rate of total loss declarations hit an all-time high of 27%. A major factor is that modern cars are filled with expensive sensors and safety technology that are costly to repair or replace. You can learn more about this trend at GM Authority.

Why This Calculation Matters to You

Once your vehicle is officially totaled, the entire focus shifts to its total loss car valuation. The insurance company’s next step is to calculate its ACV, and that number becomes the basis for their settlement offer.

This valuation directly impacts how much money you receive to buy a replacement vehicle. If the insurer’s ACV is too low, you won’t have enough to purchase a comparable car, forcing you to cover the difference out of pocket. This is why it’s critical to challenge their valuation and ensure it’s fair and accurate.

How Insurers Determine Your Car’s Value

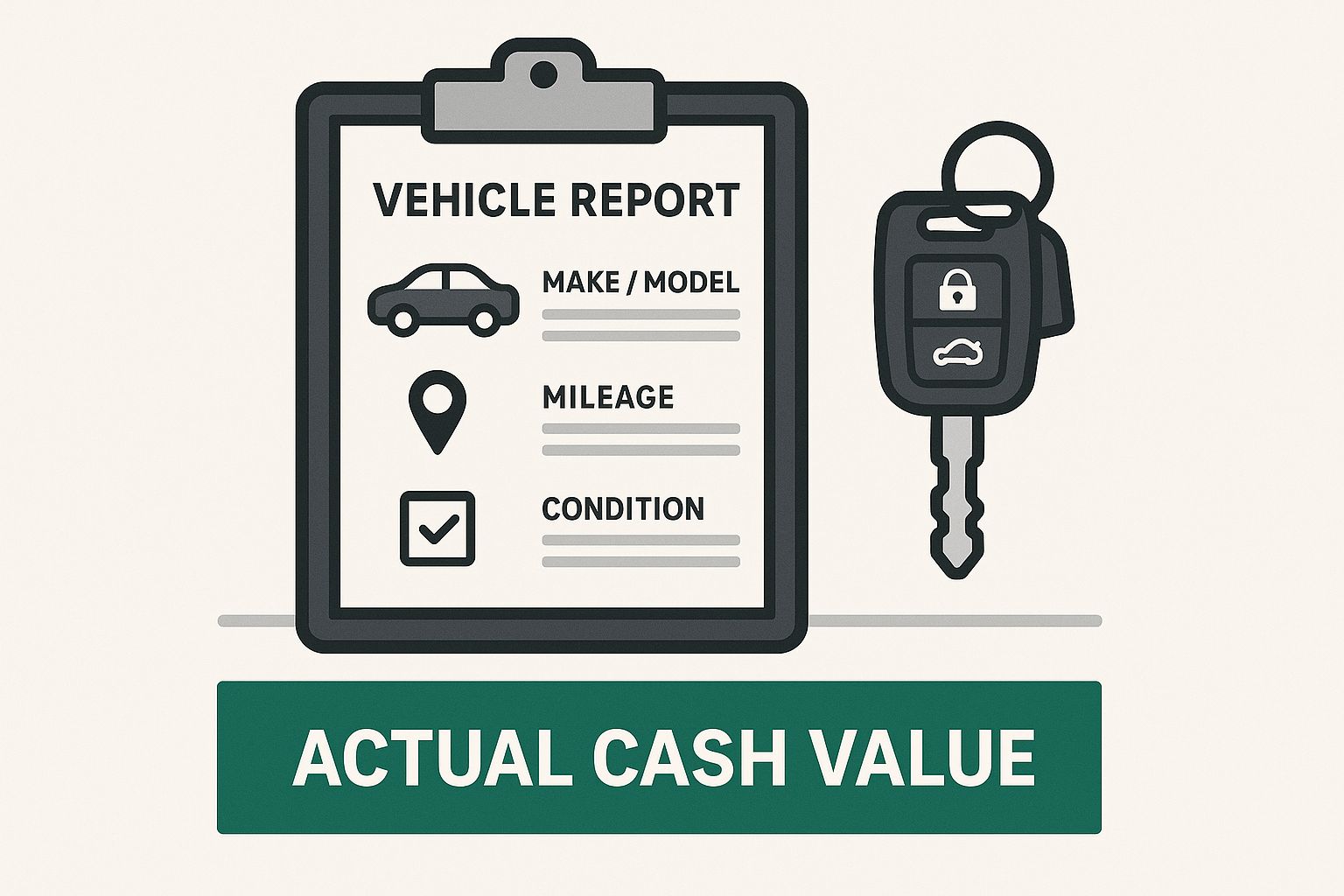

When a car is declared a total loss, the insurance company begins the total loss car valuation process. Their goal is to determine its Actual Cash Value (ACV)—what your vehicle was worth on the open market just before the accident. This number is the foundation of their entire settlement offer.

ACV is not what you paid for the car, nor is it the cost of a brand-new replacement. Instead, ACV represents the price a willing buyer would have paid for your specific car in its exact pre-accident condition. To arrive at this figure, insurers rely on automated valuation systems.

The infographic below shows how ACV is the core of a vehicle valuation report, representing its true market worth before the crash. You can learn more about experience of reditters about how is total loss settled.

Understanding the factors that influence your car’s ACV is essential when you’re facing a total loss claim.

The Role of Third-Party Valuation Systems

Most major insurance carriers don’t perform these valuations in-house. They outsource the task to large data companies like CCC ONE or Mitchell International. These platforms are essentially massive databases that constantly analyze vehicle sales data from across the country.

Here’s how they work: The system searches for “comparable” vehicles—or “comps”—that recently sold in your local area. It looks for cars of the same make, model, and year to establish a baseline value. From there, it makes adjustments based on your car’s specific details.

Key Takeaway: The insurer’s valuation is not a handmade appraisal from an unbiased expert. It’s an automated report generated by a computer, which often leads to mistakes and lowball offers.

Key Factors in the ACV Calculation

The automated system is programmed to adjust the baseline value based on several key data points. Even seemingly minor details can significantly affect your final total loss car valuation.

The table below outlines the primary factors that determine your car’s ACV. These are the exact items the insurance company’s report will analyze, and understanding them empowers you to spot inaccuracies in their offer.

Key Factors Influencing Your Car’s Actual Cash Value (ACV)

| Valuation Factor | What It Means for Your Car | Why It Impacts Your Payout |

|---|---|---|

| Mileage | Your odometer reading compared to the average for its age. | Lower mileage typically increases value, while high mileage reduces it. A significant difference from the average will trigger a major adjustment. |

| Condition | The vehicle’s pre-accident cosmetic and mechanical state, often rated from poor to excellent. | This is highly subjective. A low condition rating can deduct thousands from your offer and is a frequent point of dispute. |

| Trim Level & Options | Factory-installed features like a sunroof, premium audio, leather seats, or advanced safety tech. | A fully loaded model is worth much more than a base version. The system must account for every factory option to be accurate. |

| Recent Upgrades | Major investments like new tires, a replaced transmission, or significant engine work. | These can add substantial value, but only if you have receipts. Without proof, insurers will likely ignore them. |

Ultimately, this automated process is designed for the insurer’s efficiency, not your benefit. It can easily overlook what made your car unique, such as immaculate condition or a rare, in-demand color.

Where Automated Valuations Go Wrong

Because these systems are algorithms that rely on available data, mistakes are common. The “comps” they use may not be truly comparable. For example, they might use base models to value your top-tier trim or pull sales data from a different region where cars sell for less.

Condition adjustments are another major problem. An adjuster who has never seen your vehicle might simply assign an “average” condition rating based on its age, unfairly lowering its value without evidence. Knowing the true value of a totalled car requires you to scrutinize the insurer’s report and question these details. This is precisely why you should never accept the first offer without doing your own research.

Why Your First Insurance Payout Offer is Often Too Low

After your car is totaled, the insurance company will send a settlement offer. It’s crucial to remember this first number is usually a starting point for negotiations—and it’s often much lower than what your vehicle was actually worth.

This isn’t necessarily an act of bad faith. More often, it’s the result of the automated systems insurers use to generate valuations. These platforms are built for speed, not for capturing the unique qualities of your car. They can easily miss important details, leading to a flawed total loss car valuation that leaves you underpaid.

Mismatched Comparable Vehicles

The most common reason for a low offer is the use of poor “comparable” vehicles, or “comps.” The insurer’s software uses data from recently sold cars that are supposed to be similar to yours. The problem is, the system frequently gets this wrong.

For example, perhaps your car was a top-of-the-line trim with a premium sound system, a sunroof, and advanced safety features. The valuation system might unfairly compare it to base models that sell for thousands less, immediately lowering your settlement value.

Overlooked Upgrades and Maintenance

Did you recently invest in your vehicle? The insurer won’t know unless you provide proof. Their automated systems have no way of knowing you just spent $1,200 on new tires or had major engine work done last year.

These investments add real value, but they are almost always missing from the initial valuation. To get credit for them, you must provide receipts and maintenance records. Without documentation, the value you added simply vanishes from their calculation.

Unfair Condition Adjustments

One of the most subjective—and disputable—parts of a valuation is the “condition adjustment.” An adjuster who has likely never seen your car will assign it a rating like “fair” or “average” based on little more than its age and mileage.

Key Takeaway: An unfair condition rating is a huge red flag. If you meticulously maintained your vehicle, a generic “average” rating could be costing you thousands of dollars.

This is a classic failure of automated systems. They can’t account for the owner who kept their car spotless and followed the service schedule perfectly. If their report lists deductions for minor wear that didn’t exist, you have every right to push back. A great first step is learning about the process of disputing a total loss offer so you’re fully prepared.

How to Spot the Red Flags

When you receive the insurer’s valuation report, don’t just look at the final number. Scrutinize every detail. Ask yourself these questions:

- Are the Comps Truly Comparable? Check the trim level, options, and mileage. Do they actually match your vehicle?

- Is My Car’s Condition Represented Accurately? Did they downgrade your vehicle’s condition without a valid reason? Do you have photos proving it was in better shape?

- Are Recent Upgrades Included? Does the report credit you for new tires, brakes, or other major investments?

- Are There Unexplained Deductions? Look for any negative adjustments that seem vague or unfair and ask the adjuster to explain them.

Finding errors in these areas gives you the ammunition you need to negotiate a fairer settlement. By carefully reviewing their report and providing your own evidence, you can build a strong case for what your vehicle was truly worth.

Building Your Case for a Fairer Total Loss Payout

Receiving a lowball offer on your total loss car valuation is frustrating, but you don’t have to accept it. Challenging the insurer isn’t about arguing—it’s about building a case with undeniable facts. Your goal is to present evidence so compelling that the adjuster has no choice but to increase their offer.

Think of it this way: the insurance company has presented their side with their valuation report. Now, it’s your turn to tell the real story, backed by solid proof.

Gather Your Essential Documents

Before contacting the adjuster, assemble your evidence. These documents create a detailed picture of your car’s history and condition—details an automated valuation system often misses.

Start by collecting the following:

- Maintenance Records: Every oil change receipt and service invoice is valuable. A consistent service history proves the vehicle was well-maintained, directly challenging a low condition rating.

- Receipts for Recent Upgrades: Did you install new tires or replace the brakes recently? Any money you’ve invested adds value, but you must prove it with receipts.

- Original Window Sticker: If you have it, the original sticker is gold. It lists every factory-installed option, ensuring you get credit for a higher trim level the insurer may have overlooked.

- Pre-Accident Photos: A few photos or a video showing your car in great condition before the crash can be incredibly powerful. They can instantly counter an unfair “average” or “fair” condition rating.

Find Your Own Comparable Vehicles

The insurer’s report will list the “comps” they used to justify their low offer. Your next step is to find a better, more accurate set of your own. Don’t just rely on national estimators like Kelley Blue Book; find real cars for sale in your local area.

Search for vehicles of the same year, make, and model, but be specific. Look for listings that match your car’s:

- Exact Trim Level: If you had a Honda Accord EX-L, don’t let them use a base LX model as a comparison.

- Similar Mileage: Find cars with odometer readings as close to yours as possible.

- Matching Options: Look for comps with the same key features, like a sunroof or premium audio system.

Check local dealership websites and online marketplaces like Autotrader or Cars.com. Take screenshots of at least three to five strong comparable listings. This real-world market data is one of your most powerful negotiation tools. This is especially important for older cars, which are increasingly being totaled. By Q1 2024, 74% of total loss valuations were for vehicles 7 years or older, according to the CCC Intelligent Solutions Crash Course report.

The Power of an Independent Appraisal

Sometimes, even with solid evidence, the adjuster refuses to negotiate. This is where a certified, independent appraisal becomes your most effective tool. An independent appraisal is a detailed analysis from a human expert who understands the market.

A professional appraiser manually researches your local market, accounts for your vehicle’s specific condition and upgrades, and produces a defensible report designed to stand up to insurer scrutiny. It replaces their opinion with expert fact.

Using a Certified Appraisal to Strengthen Your Total Loss Claim

When your own research isn’t enough to sway the insurance adjuster, it’s time to bring in a professional. A certified, independent appraisal is the single most powerful tool for disputing a lowball total loss car valuation. It’s about arming yourself with a professional, data-driven report that provides the leverage needed to negotiate effectively.

An insurer’s valuation comes from an automated system built for volume, not accuracy. A certified appraiser, however, performs a detailed, manual analysis of your specific vehicle and its true value in your local market.

What Makes a Certified Appraisal Different?

A certified appraisal goes far deeper than the surface-level data used by insurance companies. It’s a comprehensive report built on expert human analysis and solid market evidence.

A professional appraiser will:

- Conduct Hyper-Local Market Research: They investigate your specific geographic area to find truly comparable vehicles, ensuring the data reflects what cars like yours are selling for right now, where you live.

- Account for Unique Features: Every detail is considered, from rare factory options and aftermarket upgrades to your car’s specific condition and maintenance history.

- Provide a Defensible Report: The final document is built to withstand scrutiny, with clear justifications for its valuation that an adjuster cannot easily dismiss.

This level of detail is critical. The used car market is complex, and values can shift quickly. For example, recent data showed that while battery electric vehicle (BEV) values dropped 1.70% in one quarter, mild hybrids increased by 1.62%. You can read more about these vehicle value trends on Repairer Driven News. A certified appraiser understands these nuances.

From Opinion to Objective Fact

Presenting an independent appraisal transforms the negotiation. You are no longer just pitting your opinion against the insurer’s. You are providing objective, third-party evidence from a qualified professional, forcing the adjuster to address the facts.

A certified appraisal report from a trusted source like SnapClaim provides the impartial, data-backed proof needed to move your negotiation from a stalemate to a successful resolution.

At SnapClaim, our team of certified appraisers creates court-ready reports that give you the confidence to demand fair compensation. We specialize in preparing a detailed total loss appraisal that methodically deconstructs the insurer’s low offer and rebuilds your car’s value based on credible evidence.

A Risk-Free Step Toward a Fairer Payout

We understand that paying for an appraisal can feel like a risk when you’re already facing a financial loss. That’s why we stand by our work with a simple promise.

SnapClaim’s Money-Back Guarantee is straightforward: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed. This makes getting expert help a risk-free decision. You have nothing to lose and potentially thousands to gain by arming yourself with the proof needed for a fair settlement.

FAQ: Common Questions About Total Loss Car Valuation

Can I keep my car if it’s a total loss?

Yes, in most states, you have the option to keep your vehicle, a process called “owner retention.” The insurance company will pay you the car’s Actual Cash Value (ACV) minus its salvage value (what they would get for it at auction). However, the car will be given a “salvage title,” which makes it difficult to insure and drastically reduces its resale value. You will be responsible for all repairs and passing a state inspection before it can be re-titled as “rebuilt.”

What if I owe more on my loan than the total loss payout?

This situation is called being “upside down” on your loan. If the insurance payout is less than your loan balance, you are responsible for paying the difference to the lender. This is where Guaranteed Asset Protection (GAP) insurance can help. If you purchased GAP coverage, it is designed to pay off this exact difference, so you don’t owe money on a car you no longer have.

How long does a total loss claim take?

The timeline can vary, but it often takes several weeks from the initial inspection to receiving a check. The process includes the valuation, the offer, any negotiations, and final paperwork. You can help speed things up by responding promptly to your adjuster and having your title and loan documents ready.

Do I have to accept the insurance company’s first offer?

Absolutely not. The first offer is a starting point for negotiation, not a final decision. You have the right to review the insurer’s valuation report, question their findings, and present your own evidence—such as maintenance records and comparable vehicle listings—to support a higher car value after accident. A certified appraisal provides the strongest proof to strengthen your claim for a fair insurance total loss payout.

SnapClaim is ready to help you prove your vehicle’s true worth. Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

https://www.snapclaim.com

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This article was reviewed by SnapClaim’s team of certified auto appraisers and claim specialists with years of experience preparing court-ready reports for attorneys and accident victims. Our content is regularly updated to reflect the latest industry practices and insurer guidelines.

Get Started Today

Ready to prove your claim? Generate a free diminished value estimate in minutes and see how much you may be owed.

👉 Get your free estimate of your total loss vehicle.